Thank you for the opportunity to share with you the evolution of New Zealand's currency. Realistically there are many people here who will have a much deeper breadth and depth of knowledge on the history of currency in New Zealand than I do. So in recognising that, I intend to briefly summarise our ‘past evolution' and focus more on the next stage of evolution.

The early steps for New Zealand currency

Until the mid-nineteenth century, most coins and banknotes were British and there were some transactions made with promissory notes.[1]

There was no central issuing authority, and from 1857 until the 1880s tradesmen's tokens were circulated in New Zealand by over 40 mercantile firms, companies and individuals as money, like ordinary coins, when there was not enough small change in circulation. They were not officially authorised by the governments of the day and were never legal tender but they were widely accepted by the general public because of their convenience. The use of tokens died out in the 1880s when the supply of Imperial coinage increased greatly.

From the mid nineteenth century through to the early twentieth century, banknotes produced by trading banks were in common circulation. Banks were not obliged to accept each other's notes, though most did in practice, and it was 1924 before they reached an agreement on a uniform design.

Figure 1: New Zealand Banknotes 1934 - 2015

After years of debate, the decision to set up a central bank was made in 1932 with sole authority to issue New Zealand's currency. Work to design new banknotes began in December 1933, and they were issued in August 1934, when the Reserve Bank started operations (see Figure 1). The first notes were intended to be temporary. They had been designed in haste amid heated debate over what they should look like. In the end, the notes included features of the Bank of New Zealand notes already in circulation.

The second issue appeared in 1940, timed to coincide with the Treaty of Waitangi centennial. These notes retained the earlier colours but introduced quite different designs. A new green 10 pound note was also introduced, and these note designs remained in circulation until the change to decimal currency in 1967.

In 1959, a committee was set up to study and report on decimal currency. This committee was in favour of adoption, and after further study, it was announced in 1963 that New Zealand would change to a decimal currency system. The Decimal Currency Act, 1964 prescribed the designs, diameters, and standard weights of the decimal coins, which first appeared in circulation on 10 July 1967.

The New Zealand Dollar series became the third banknote series. This series featured H.M Queen Elizabeth on the face of all denominations.

In 1981, the fourth series was launched largely as a result of a 1979 decision to change printer to Bradbury Wilkinson & Company in Whangarei. The only major artistic change was an update of the portrait of the Queen. A new denomination note, the 50 dollar note, was introduced as part of the fourth series in December 1983.

In 1991, the Reserve Bank decided to modernise the currency, and after wide consultation the note designs were changed for series five, bringing prominent New Zealanders and iconic flora and fauna more strongly to the fore.

In 1999 the designs were slightly modified when the bank launched the current series six flexible plastic polymer notes.

Through our note history, the Reserve Bank has retained design and intellectual property right independence, while working in close collaboration with specialist printers in New Zealand, the United Kingdom and Australia, and mints in the UK and Canada. In terms of innovation, the Bank has been an early adopter of the use of polymer substrate and the wholesale distribution model for distributing and fitness sorting of banknotes. As a result, the Bank has delivered a cost-effective currency operation which meets the needs of the public.

The recent evolution of coins

The Treasury was responsible for coin issuance until 1989 when responsibility was transferred to the Reserve Bank. The Reserve Bank quite quickly withdrew the 1 and 2 cent coins. They stopped being legal tender in early 1990. The decision to introduce 1 and 2 dollar coins was made in 1986, and they were introduced in 1991, replacing the 1 and 2 dollar notes. The Royal Mint in the UK continues to mint these coins.

In 2006 lighter, plated steel 10, 20, 50 cent coins were introduced and the 5 cent coin was taken out of circulation. These were minted by the Royal Canadian Mint, and the Bank has continued that relationship.

Regarding the evolution of currency in New Zealand, there has been a ‘theme' of innovation which is worthy of note as it reflects one of our organisation's values.

The Reserve Bank has historically had close links with the UK in the procurement of currency. This expanded to a wider commonwealth flavour in 1999 with the use of Note Printing Australia (NPA)[2] to produce a new generation of polymer banknotes, following on from the Reserve Bank of Australia's (RBA) pioneering endeavour. NPA produced a very innovative and durable banknote for the day, and New Zealand has been served well by series six, now lasting 15 years. This commercial relationship is now about to close with NPA focusing on the RBA's new series and not participating in the Reserve Bank of New Zealand's tender process for the next series of banknotes.

The innovation theme was also at the forefront of the ‘silver coin' change out in July 2006. The development of smaller, lighter and lower-cost plated steel coins, and the removal of five cent pieces from circulation, gave New Zealand a coherent and logical set of coins that were more convenient for the public, easier for those handling coin in bulk, such as banks and security firms, and less costly to manufacture, saving the taxpayer.

The modernisation was based on a patented electroplating process which allowed a complex electromagnetic signature to be available for the coin vending industry for identifying and authenticating coinage.

The steel-plated coins remain a high quality, durable and cost effective currency solution, with The Royal Canadian Mint being an important partner in innovation development.

Preparing for the next evolution of currency in New Zealand

The Reserve Bank publishes its strategic priorities in its Statement of Intent. One of the ten organisational priorities in the 2013-2016 Statement of Intent, was to re-examine the Bank's currency function in order to prepare the business for the pending release of a new series of banknotes and the subsequent growth in operational activity.

Over the last year that has effectively entailed the preparation of the Wellington facilities for a large increase in activity when the next series of banknotes is released and ensuring the Bank has the processing capability in place to handle two banknote series.

In preparing for the next series, the Bank has taken a much more ‘hands on' role in the design and product specifications of the new series. Series seven is primarily about improving the integrity and security features of the current ‘family' of notes. Early on in the project the Bank decided to retain control of the selection of security features and ensure that they incorporated a strong New Zealand influence that will resonate with the public.

New technologies and the ability to collaborate with other central bank technical staff have enabled the Reserve Bank to identify best practice in terms of product design and production capability. Through procurement and outsourcing processes, we have been able to identify printers who have the proven capabilities in providing banknotes with strong aesthetics and high quality security features, while maintaining banknote integrity and durability.

The technology for designing and printing banknotes has advanced considerably since the current series were first issued in the early 1990s, and while counterfeiting rates in New Zealand are low compared to other countries[3], we need to stay one step ahead of the game.

The security features that are built into banknotes are an important element of guarding against counterfeiting. When the series six notes were introduced in 1999, it was generally considered that New Zealand currency was well protected against counterfeiting due to the difficulty of printing on polymer substrate. While that has proved to be the case, since 1999, there have been significant advances in copying, scanning, and printing technologies and reductions in capital costs. As a consequence the economics of counterfeiting have changed substantially and the risk of counterfeiting has increased. Counterfeiting risk, if realised, carries many associated costs including loss of confidence in the nation's currency and its economic and public sector management, and loss of confidence in the Reserve Bank. Improving banknote counterfeit resilience is a sound preventative maintenance practice for central banks.

The Bank of Canada and the Bank of Mexico have experienced significant counterfeiting attacks within the last decade. The Reserve Bank of Australia has also previously been affected by a small number of professional counterfeiting operations, and is itself preparing a new banknote series in order to lower risks.

In addition to the security aspects, the current banknote designs are now 21 years old. Printer technology and inks have advanced significantly over that time, particularly those applied to polymer. Upgrading the notes is a chance to refresh and enhance the image of New Zealand's currency by taking advantage of this improved technology. The new series is designed to provide highly visible security features for the public while incorporating a new generation of machine readable security features.

The future of cash in New Zealand

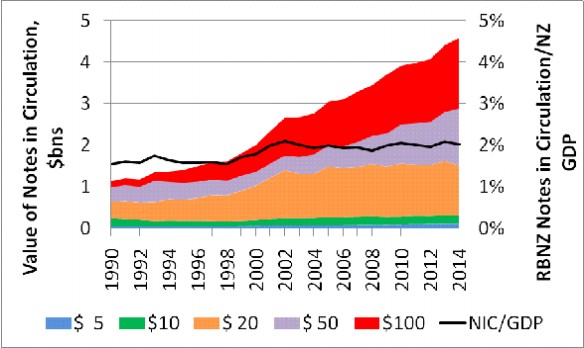

There have long been predictions of the demise of cash in society. Yet, the consistent growth of notes in circulation at 4.6 percent per year (in terms of note value; 2.5 percent per annum in terms of number of notes) has undone many such predictions of a fall in demand. Currency issued has grown by over 6 percent in the past year. Notwithstanding perceptions of the ‘end of cash', the demand for cash has continued to grow, pretty much in line with the growth in the nominal economy. In New Zealand, notes in circulation rose from 1.5 percent of GDP in 1990 to 2 percent in 2001 and have remained about that level since.

This growth has been mirrored in many other countries in recent years. In the UK, notes in circulation have grown by 6 percent per year since 1990, increasing from 2.4 percent of GDP in the mid 1990s[4] to over 3.5 percent in 2013. The growth over the last twenty years arrested and partially reversed a long-term decline from almost 8 percent of GDP in 1960.[5]

Increased demand for cash is surprising given the growth of electronic payments. New Zealand has a very high penetration rate for electronic payment, with 280 debit or credit card transactions per person in 2013, which is exceeded only by Iceland and Norway[6]

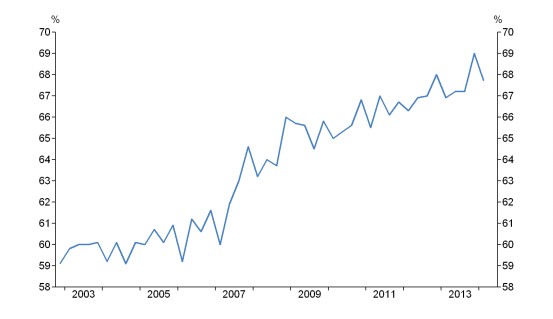

The share of electronic card transactions in the core retail industries has been increasing slowly over time. The mean share of the core retail spending[7] (excluding GST) in the December 2013 quarter was 69 percent, compared with 59 percent in December 2002[8]. Moreover the average dollar size of transactions has been declining, suggesting greater use of cards for small transactions that cash may previously have been used for.

Figure 3: Share of core retail spending by electronic card

transactions

(quarterly, excluding GST)

Banknotes have multiple uses. The transactional, means-of-payment use is just one of them. Indeed, this particular use may well be declining given the rising tide of electronic payment. Some central bank estimates suggest that the proportion of cash in circulation used for day-to-day transactions is as low as 30 percent[9].

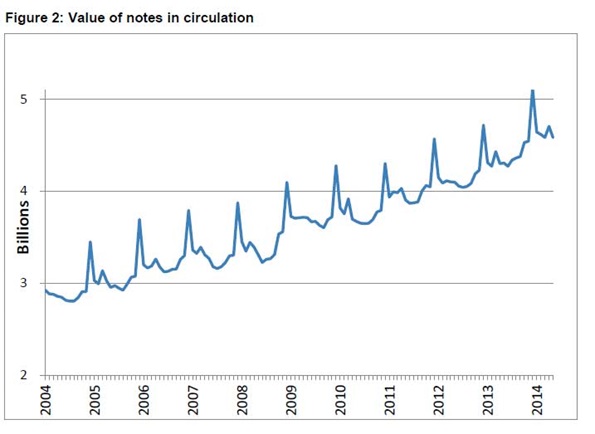

Figure 4: Reserve Bank banknotes in circulation

Other uses include:

- overseas holdings (by offshore residents) – either in anticipation of tourism travel and spending in New Zealand or as a store of value, or perhaps as a hedge against their own currency risk. There is evidence to suggest this may be a driver of cash demand, with visitors to New Zealand increasing from 1.7 million in the year to June 2000 to 2.8 million in the year to May 2014.

- domestic hoarding as a store of value – perhaps against natural disaster risk or electronic payments failure, or financial institution failure, or simply as a means of saving. Low interest rates on deposits that reduce the opportunity cost of holding cash may have contributed to the recent growth in notes demand. Failures of finance companies domestically and banks internationally may also have contributed to a perceived safe-haven value of cash holdings.

- the shadow economy – facilitating illegal transactions e.g. drug trade, or evading taxation through cash payments.

In New Zealand, the expanded circulation of notes through ATMs appeared to drive a lift in 20 dollar notes in the late 1990s, while a shift towards 50 dollar note dissemination appears to underpin a significant growth in cash in the past year. ATM distribution supports multiple uses and does not by itself make it possible to distinguish motives.

That said, more rapid growth in larger denomination notes (20 dollar, 50 dollar and 100 dollar notes, see Figure 4) tends to support arguments that these store of value, overseas and possibly black economy purposes have been key drivers of note demand.

While commercial sector (banking and industry) issuance of currency was common in the nineteenth century around the world, and continues in some countries today, generally it has been the preserve of the state and central banks since their institutional rise in the twentieth century. Recently, there has been a challenge to the form and provenance of money. Virtual currencies, of which the best known is bitcoin, have been created as an alternative means of payment and store of value. It is a very low cost payment method with strong security features and usable for cross-border transactions, making it advantageous in some regards relative to more traditional payment mechanisms.[10]

As compared with cash, however, crypto-currencies currently have a number of drawbacks. In a transactional sense, their use is limited by the number of businesses willing to accept them for payment, currently a very small number. Large swings in the value of a Bitcoin means its purchasing power fluctuates considerably, and the finite number of Bitcoins possible mean that their scarcity value tends to make them more like speculative investment commodities than transactional payment instruments.

While bitcoins or other crypto-currencies are unlikely to replace cash in the foreseeable future, technological change is relentless and there is nothing innate about cash-money that says it must continue forever[11]. Key attributes of trust (that the "money" gives rise to settlement of the obligation) and anonymity (it is often efficient for the sale/purchase parties not to have to identify one another) must be met, but if these can be accomplished reliably and sustainably new technologies could supplant cash as we know it in years to come. Central banks need not be overwhelmed by such innovations[12]. As they have to date, central banks around the world will need to monitor and develop their regulatory and currency operations roles to meet developments in technology, and the changing needs of the public.

The next steps in the evolution of New Zealand's currency

The Reserve Bank is committed to evolving products and services in line with and in anticipation of future currency demands. While other means of payment keep growing, cash remains in strong demand, and we need to keep it current and viable for its users.

The evolution of New Zealand's banknotes will take another step at the end of next year, when our next series of banknotes starts to enter circulation.

In 2011 we launched a banknote upgrade project to make sure our banknotes would benefit from technological advances in security features. To ensure we really understood just how much banknote design and print market has advanced in the last few decades, in 2013 we ran a multi-stage international tender process and attracted proposals from around the world.

Separate tenders were issued for banknote design and print contracts. Seven submissions were received for design and five for print. Recently, contract negotiations were completed with the preferred company which coincidently submitted both the successful design and print proposals.

We have selected Canadian Banknote Company to design and print New Zealand's banknotes for a five year period. Canadian Banknote Company has a strong reputation for technologically advanced printing, and currently manufactures New Zealand's passports. It also prints the Bank of Canada's banknotes. We're confident it will deliver high quality banknotes which New Zealanders can continue to identify with and trust.

With the focus of the banknote upgrade being to improve and update security features, we're not changing the New Zealanders or the flora or fauna depicted on the notes. Our research shows that the public generally like the design of the existing banknotes, particularly the New Zealand themes[13]. Given the technological advances in the printing process, we expect the new notes will have a more modern look, finer detail and improved colour.

The notes will contain more sophisticated security features that will greatly enhance the overall design. The notes will continue to feature transparent windows, as with the current series. However, these will feature a greater level of both design and security. Several other security features will be added, including colour changing and optically variable features.

We will also improve design features to help visually impaired people identify the notes, and differentiate the denominations.

Subject matter experts, industry manufacturers and focus groups are being consulted during the development of designs to ensure that the public will have confidence in the refreshed designs.

There are many variables and risks in the conversion of a design into a printed banknote too. We expect to publicly release the ‘near final' designs in November, after they have been tested to ensure the designs are viable, and can be printed successfully in a robust, secure and durable manner; and they can be accommodated by businesses, retailers, banks and others key users such as banknote equipment manufacturers.

New Zealand has seen a proliferation of currency handling equipment deployed since the launch of series six in 1999, e.g: accepting and dispensing ATMs, kiosks, teller cash recyclers, gaming, vending and parking machines.

There is a lot of other behind-the-scenes work going on in preparation for the release. Shortly we will begin consultation with technical stakeholders to determine the optimum way to release the notes, but it is likely we will release two denominations in the fourth quarter next year, and the remaining three denominations about six months later. Both series will be legal tender, so people can continue to use both series.

An education campaign will be run to familiarise the public and businesses with the new notes before they come into circulation, so we can ensure a seamless transition.

From a financial perspective the bank has completed early forecasts of possible release and co-circulation scenarios. At a high level, the Bank spends approximately $5 million per annum on notes, and is preparing for incremental (operating) costs as a result of the new series of $43 million over the next five years.

A firmer expense estimate will have to wait until industry consultation is completed over the next four to six months on release and repatriation strategies. Even with industry collaboration, considerable uncertainty will remain on how quickly the public will repatriate the old notes. While we have observed international experience, New Zealand has a history of relatively quick currency upgrades when benchmarked with peers.

A new series will provide the Bank with new opportunities in banknote quality assurance, with new technologies becoming available in note processing detectors and remote data capture. A banknote could soon be tracked and quality assessed in remote processing facilities, which has potential impacts across the industry. The Reserve Bank note processing machines may not be the primary assessor of note quality or authenticity as has traditionally been the case.

The Reserve Bank is looking closely at these new technologies and working with the industry to better understand how they are operating in the New Zealand context. Mechanisation and data analysis are becoming the future of currency management.

Other product development and innovation

Coins are also an interesting area for innovation. The Royal Canadian Mint, who produces our 10 cent, 20 cent and 50 cent coins, continues to evaluate new opportunities for innovation. In the June 2014 Currency News, they revealed significant improvements in high-speed minting technology, which will ‘revolutionise' coloured circulating coins. This opportunity, which could be a first for New Zealand, is currently under evaluation by the Bank's currency staff. The bank continues to evaluate unique opportunities to celebrate our heritage, and encourage a new generation of numismatists.

The Gallipoli centenary will take place next year and we are looking at opportunities with New Zealand Post to mark this occasion.

As you all will appreciate, currency in circulation represents an important part of the New Zealand brand, which resonates with New Zealanders and the people who visit. It says something about who we are, and how we see ourselves. Innovation is central to the New Zealand culture, and is also important to the Reserve Bank. With this in mind, we will find new ways to celebrate New Zealand in our currency while preserving the core integrity, functionality and confidence in the product.

New Zealand currency is an evolving journey and we are looking forward to sharing that with you all in 2015 and into the future.

[1] Reserve Bank of New Zealand, "Explaining New Zealand's Currency".

[2] NPA is wholly owned by the Reserve Bank of Australia.

[3] Counterfeiting rates in New Zealand are below our target of having less than 10 counterfeits per million notes in circulation. The rate reached 18ppm in 2002, but fell considerably afterwards, and remains low – less than 1 ppm in 2012-2013.

[4] Andrew Bailey (Bank of England), Speech: ‘Banknotesin circulation: Still rising: What does this mean for the future of cash?' December 2009.

[5] Helen Allen, Andrew Dent (Bank of England), ‘Managing the circulation of banknotes' in Quarterly Bulletin, Q4, p302 -210. 2010.

[6] ‘Developmentsin retail payment services – 2013', Norges Bank Papers, No.1, 2014, page 9.

[7] Core retail excludes the four vehicle-related industries.

[8] Statistics New Zealand, Electronic Card Transactions, May 2014.

[9] ‘The use of Euro banknotes – Results of two surveys among households and firms'. ECB Monthly Bulletin. April 2011.

[10] Anders Laursen and Jon Hasling Kyed, ‘Virtual Currencies', Danmarks National Bank Monetary Review 1st Quarter 2014.

[11] Felix Martin. Money – The Unauthorised Biography. The Bodley Head, Random House. 2013.

[12] Andrew G. Haldane (Bank of England) and Jan F. Qvigstad (Norges Bank), "The evolution of Central Banks - A Practitioner's Perspective", May 2014.